From the first day you live or work in the Netherlands, you are building a pension. Most expats don’t know this — or they do, but it feels so far away that they ignore it. This guide explains how the Dutch pension system works in 2026, how much you can expect to receive, what happens if you return to your home country, and what you can do right now to improve your financial future at retirement.

Key numbers at a glance — 2026

- Retirement age in 2026: 67 years (unchanged until 2027)

- Maximum AOW (state pension) for a single person: €1,662.16 gross/month

- Maximum AOW for a couple: €1,139.39 gross/month per person

- The system has three pillars: state pension + employer pension + individual pension you control

- If you arrived in the Netherlands after age 17, you will not receive 100% of the state pension — there is a clear formula to calculate your entitlement

- If you return to your home country, the state pension can be paid abroad — but with conditions depending on the country

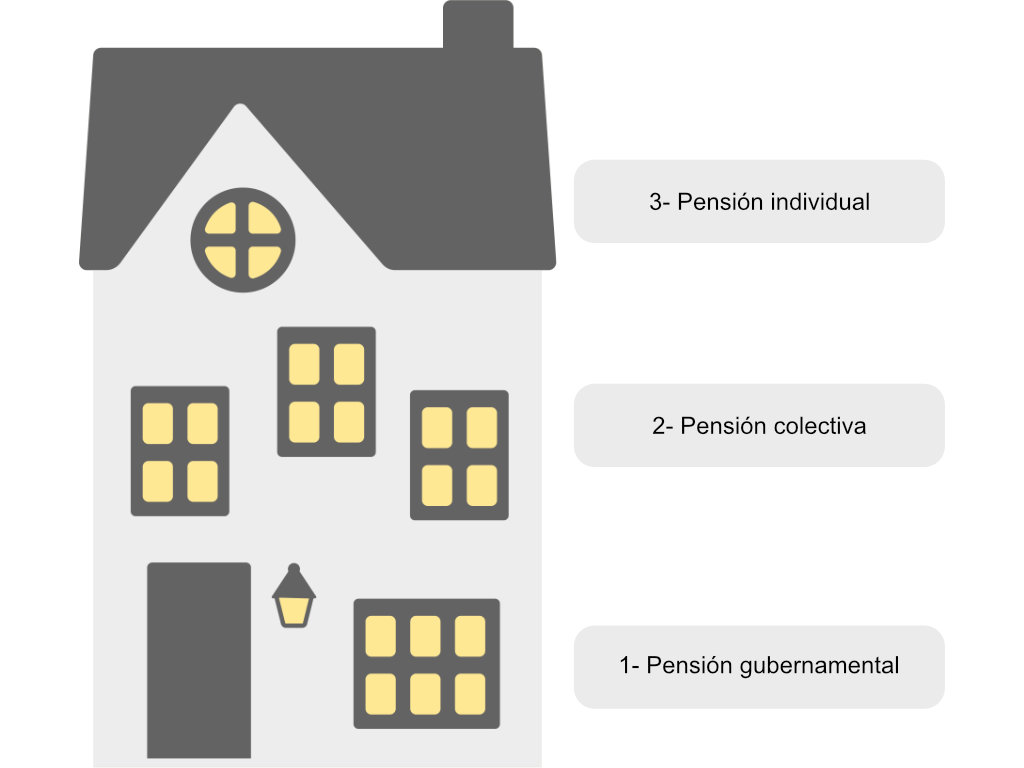

The three-pillar system

The simplest way to understand the Dutch pension system is to imagine a three-floor house. When you retire, your total pension will be the sum of the floors you have built:

- Ground floor — AOW: the state pension. Accumulated automatically by living or working in the Netherlands.

- First floor — Collective pension: built through your employer. If you work as an employee, you are almost certainly accumulating this without realising it.

- Second floor — Individual pension: the one you build voluntarily, with tax advantages.

In most Latin American countries, only the equivalent of the ground floor exists. In the Netherlands, all three can add up, which makes the final pension substantially higher than in most other systems.

| Example 1 (recently arrived) | Example 2 (employee) | Example 3 (full plan) | |

|---|---|---|---|

| 1. AOW (state pension) | €1,400 | €1,750 | €1,662.16 |

| 2. Employer pension | €0 | €1,200 | €1,500 |

| 3. Individual pension | €0 | €0 | €800 |

| Total monthly | €1,400 | €2,950 | €4,432 |

Ground floor — AOW: the Dutch state pension

How is it accumulated?

The AOW (Algemene Ouderdomswet) is the basic state pension. It accumulates at a rate of 2% for every year you live or work in the Netherlands, over the 50 years before retirement age — that is, between ages 17 and 67.

Someone who has lived in the Netherlands from age 17 to 67 accumulates 100% of the AOW. If you arrived later, the percentage is lower:

| Age when you arrived | Years in NL until 67 | AOW entitlement |

|---|---|---|

| Age 22 | 45 years × 2% | 90% |

| Age 25 | 42 years × 2% | 84% |

| Age 30 | 37 years × 2% | 74% |

| Age 35 | 32 years × 2% | 64% |

| Age 40 | 27 years × 2% | 54% |

Every year you remain in the Netherlands adds 2% more, regardless of whether you are employed or not — simply living here counts.

How much do you receive in 2026?

The gross AOW amounts from 1 July 2026 are:

| Situation | Gross AOW/month | Holiday allowance/month |

|---|---|---|

| Single / living alone | €1,662.16 | €104.78 |

| Couple (per person) | €1,139.39 | €74.85 |

The vakantiegeld (holiday allowance) accumulates throughout the year and is paid in a lump sum in May. The net amount you actually receive depends on your tax situation, but for a single person with loonheffingskorting, take-home pay is typically around €1,500–€1,600 net/month.

You can check exactly how much you have accumulated — combining all three pillars — at mijnpensioenoverzicht.nl. You need your DigiD to log in.

At what age do you retire in the Netherlands?

The AOW retirement age in 2026 is exactly 67 years. It stays at 67 in 2026 and 2027. From 2028 it will rise to 67 years and 3 months, and will continue increasing linked to life expectancy (for every year life expectancy increases, the AOW age rises by 8 months).

You can calculate your exact retirement date at svb.nl.

What if you return to your home country?

The AOW is paid by the SVB (Sociale Verzekeringsbank) and can be received while living outside the Netherlands — but with conditions:

- EU countries: you receive 100% with no restrictions.

- Countries with a bilateral treaty with the Netherlands: you receive 100%. Spain, Colombia and several other Latin American countries have treaties. Check the full list at svb.nl.

- Mexico: no bilateral treaty with the Netherlands, so the SVB pays only 50% of the AOW if you reside permanently in Mexico.

- Other countries without a treaty: the SVB applies a reduction. Check your specific country before making decisions.

First floor — Employer pension (collective pension)

If you work as an employee in the Netherlands, you are almost certainly accumulating an additional pension through your employer. Your employer pays a monthly contribution to a pension fund or insurer — and you also contribute a portion deducted from your salary.

The new system: Wet toekomst pensioenen

In 2023, the Wet toekomst pensioenen (Pensions Future Act) came into force — the most significant reform of the Dutch pension system in decades. The transition for most pension funds runs until 2028.

The key change: the system moves from defined benefit (you knew exactly what you would receive) to a personal account model where you can see exactly how much money you have accumulated. The money is invested and grows (or may fall) in line with financial markets — more transparent, but with more variability.

For workers who arrive in the Netherlands and change jobs frequently, this is good news: the money accumulated stays in your personal account and you can track it at mijnpensioenoverzicht.nl even when you change employer.

What happens if you change jobs?

Each employer may have a different pension fund. When you change jobs, the money accumulated with your previous employer stays in that fund — you don’t lose it. At mijnpensioenoverzicht you can see all your funds consolidated in one place.

What happens if you move abroad?

Employer pensions are generally paid even if you move abroad, including outside the EU, though this depends on the specific fund. Contact your pensioenfonds directly to confirm the conditions for your situation.

Second floor — Individual pension (the one you control)

This pillar you build voluntarily. You open a pension account (pensioenrekening) with a bank or platform like Brand New Day, deposit money, and that money is invested in index funds. The major advantage: contributions are tax-deductible.

When you file your annual tax return (belastingaangifte), you can deduct what you have contributed within the annual limit (jaarruimte). The Belastingdienst refunds between 36% and 49% of your contributions depending on your tax bracket — essentially, the government co-funds your pension.

The money cannot be withdrawn before retirement without paying a high penalty. If you move outside the EU, there are restrictions — consult your provider before making that decision.

💡 The most popular individual pension option for expats in the Netherlands is Brand New Day — global index funds, low costs, 100% online process. Contributions are tax-deductible in your annual return, and the account can be opened in under 10 minutes.

Before deciding, it helps to read our comparison of pension accounts in the Netherlands and our step-by-step review of the Brand New Day pension account, where we explain how to open it and what it costs.

Alternative without lock-in: standard investment account

If you don’t want to lock your money until retirement, another option is to invest in a standard investment account. There are no tax benefits on contributions, but the money is yours at any time. You can read more about this in our article on investment accounts for beginners in the Netherlands.

Frequently asked questions

At what age do I retire in the Netherlands?

In 2026, the AOW retirement age is 67 years. It stays the same in 2027. From 2028 it rises to 67 years and 3 months. Calculate your exact date at svb.nl.

How much does a retiree receive in the Netherlands?

It depends on how many years you have lived in the Netherlands and how much you have accumulated across all three pillars. With a full AOW alone, a single person receives €1,662.16 gross/month in 2026. Add to this the employer pension and individual pension if you have them. To estimate your own case, use our retirement calculator for the Netherlands.

Am I accumulating a pension from the day I arrive, even if I’m not Dutch?

Yes. The AOW accumulates through residence or work in the Netherlands, regardless of your nationality. From the first day you are registered in the system, you are adding that 2% per year.

Can I receive the Dutch pension if I return to my country?

Yes, with conditions. EU countries and countries with a treaty with the Netherlands receive 100%. Mexico receives 50% due to no bilateral treaty. Check the updated list at svb.nl.

What is mijnpensioenoverzicht.nl?

It’s the official government portal where you can see a summary of all your accumulated pension: estimated AOW, collective pensions from every employer you’ve had, and individual contributions. You need DigiD to access it.

I’m self-employed (ZZP) — do I have a pension?

You do accumulate the AOW, just like any resident. But the collective pension (pillar 2) is not generated if you work as a freelancer — that part depends on employers. That’s why it’s especially important for ZZP workers to actively build pillar 3 (individual pension).

Brand New Day is especially popular among freelancers: no fixed monthly contribution required, deductible in your tax return, and low-cost index funds.

What to do now

- Check your current AOW status at mijnpensioenoverzicht.nl — takes 5 minutes with your DigiD

- Calculate your expected AOW percentage based on your arrival age (table above)

- If you are self-employed or your employer pension is small: open an individual pension account with Brand New Day and start contributing — even €100/month makes a significant difference over 20 years

- If you plan to return to your home country: check if it has a bilateral treaty with the Netherlands — this determines how much AOW you will actually receive

Related pension guides

- Retirement calculator in the Netherlands — estimate how much you’ll receive.

- Pension accounts in the Netherlands — comparison of options for the third pillar.

- Brand New Day pension account — step-by-step review and how to open it.

- My Brand New Day account — my real experience with the account.

If you have questions about your specific situation — how much you have accumulated, or what happens to your pension when you leave — leave them in the comments.